Welcome to Ganik Market Strategies LLC

Max Ganik

Equities Trader,

SMB Capital

____________________

University of Michigan

Ross School of Business

2019

Founder and Writer,

Ganik Market Strategies LLC

Option Millionaires

Director of

Diamond+ Trading Service

Staff

Market Technicians Association

Contributor, Instructor

Investopedia

Intern

TrueEX

Named #17th

“Top People in Finance to Follow on Twitter”

by TradeFollowers

Connect with

Ganik Market Strategies LLC

![]()

![]()

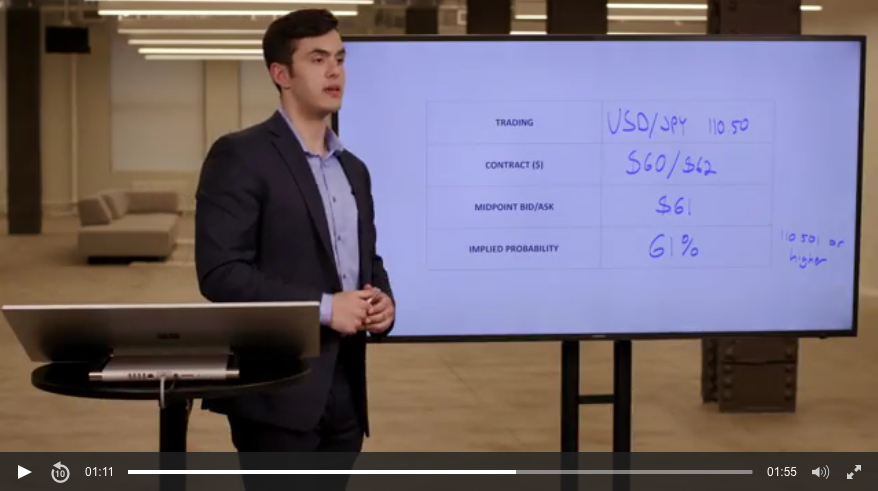

Investopedia Academy: Binary Options Trading

Binary Options can be risky, but we’ll teach you how to manage the risks and which technical indicators give you edge you need in today’s fast-moving market.

You’ll learn

-

What Binary Options Are

-

A Trading System

-

Risk management Techniques

-

Technical Indicators

-

Max’s Personal Strategies

Click HERE for more details and to register.

CNBC Fast Money Interviews with Melissa Lee

May 16, 2016:

Video Replay

Another awesome time at CNBC Fast Money, May 16, 2016

Another awesome time at CNBC Fast Money, May 16, 2016

Left to right: Tim Seymour, Karen Finerman, Steve Grass, Max Ganik, Melissa Lee, Pete Najarian

March 6, 2014:

Video Replay

What an awesome time on CNBC Fast Money, March 6, 2014

What an awesome time on CNBC Fast Money, March 6, 2014

Left to right: Dan Nathan, Tim Seymour, Max Ganik, Melissa Lee, Jon Najarian, Karen Finerman

View Max Ganik’s N.Y. Times interview on the Twitter stock, December 30, 2013:

“Rise in Twitter’s Stock Reflects Exuberance in Silicon Valley”

Max Ganik was interviewed by Mr. Pimm Fox on Bloomberg TV, December 6, 2013

Interview with Mr. Pimm Fox on Bloomberg TV

Scroll through slides below.